Good Day Traders,

Overview & Highlights: This weekend’s edition features another great article by Mike Trager. Mike’s topic as we rush headlong into the last Fed Meeting of the year is “Fang, or defanged?” which speaks to the continuing bad breadth being displayed in the Indexes. Find out what clues are showing up that could be shaping the market landscape in 2016.

The Website performance page will be updated the first full week of every month. Additionally a new video updating the performance to date of the Early Warning Alert System was recorded and is available at: https://activetrendtrading.com/early-warning-alerts-2/

Webinars: At Active Trend Trading we offer two webinars per week to provide training plus trade and market updates. See the schedule below for the next webinars.

How to Make Money Trading Stocks on December 11th

Register Here: https://attendee.gotowebinar.com/register/6593811185251424258

Next Training Webinar: Dec 9th

For Premium Members our Wednesday evening training is developing some fantastic traders!

Mid-Week Market Sanity Check Topic: Part 1: Wealth Building by Portfolio

_____________________________________________________

Managing Existing Trades: The system worked well this week in getting us out of trades that were not working well and keeping us in trades that are working fine! FB was not working so I pulled the plug rather than take the full 4% loss. NOAH gave us a good profit a couple of weeks ago but also started weakening and closed out breakeven on the last half of the shares opened. I will be seeking to fill out the full 5 stock portfolio this week if triggers and setups appear.

Strategy I: Currently 3 open trades.

Trade 1: Entered NOAH on 11/19’s pullback to the 8 day EMA. Sold ½ of the position at T1= 33.22 taking $755 in profit off the table. NOAH it the breakeven target for the last half of the trade today and closed on market weakness. Position Closed, Total Profit for this total trade: $755

Trade 2: Entered CBM on today’s pullback to the 8 day EMA. Hard Stop is placed at 4% below purchase price at 47.42. Sold ½ the position when T1 = 54.34 was triggered on 11/25. Closed 175 shares at 54.30 for a profit of $857.50

Current position up: 6.4%

Trade 3: Entered FB at 106.30 on 11/25 on a break above the 8 day EMA. At this point FB has not gotten in gear and may be a weak member of the portfolio. This would make FB the first stock to cut if a stronger candidate is identified. The action in FB today show why. Price bounced up and through and then drew back. T1 = 10% above entry at 116.93 and a Hard Stop placed as a conditional market order at 102.04. The FB trade wasn’t working so rather that hang for the fall of 4% closed the position today at 103.71 for a 2.4% loss. Position Closed, Total loss = $336.70

Trade 4: Entered NOW at 86.55 today on a bounce from the 8 day EMA on 11/30. T1 = 10% above entry at 95.21 and the Hard Stop is at 83.09.

Current position up: 3.97%

Trade 5: Entered HAWK at 47.10 on 12/3 on a bounce from the 8 day EMA. T1 = 10% above entry at 51.81 and the Hard Stop is at 45.22.

Current position up: 1.8%

Strategy II: No Open Trades

Wealth & Income Generation Strategy III Trades: If the value of the underlying Long Options plus the premium cleared from selling weekly options approaches 100% on any trade I will close the position and start a new position. With the IWM trade below because there is only 9 weeks until the long positions expire, I will look to close the total position if return approaches between 30-50%.

Trade 1: Long IWM Jan16 127C & 127P – Cleared $240 by selling call options against this position. I will be closing the underlying positions and building a 2017 position before the end of the year.

Trade 2: Long TSLA Jan17 250C & Long Jan17 220P – Waiting for Triggers

Several members have asked about this strategy and a more detailed explanation is available at: https://activetrendtrading.com/wealth-and-income-strategy/ .

I posted a video about how to choose the weekly options to short for this strategy. It can be viewed at: https://activetrendtrading.com/videos/

Additionally some of these trade may be selling weekly puts on up trending stocks. If you are interested in parallel trading this strategy register at this link: http://forms.aweber.com/form/99/1278533099.htm

_________________________________________________

Pre-Earnings Trade: 3rd Quarter earnings are just about over with a few stocks reporting during the first few weeks in December. Potential trades include: CALM, RHT & NKE.

_________________________________________________

Potential Set Ups for this week: I would like to fill out the final 2 stocks for Strategy I this week plus add to CBM if possible. If the market does provide a Santa Claus rally (which may take place after the Fed) then having great stocks in the corral will a great way to finish the year.

Upside: Add to CBM. NOAH, AKRX (the fundamentals on this one are mixed but it has had a very strong move over the past few weeks),

Downside: MBLY, AFSI & FIT

On the Radar: TSLA, NOAH, NFLX, PANW, DATA, LNKD, HAWK, EPAM, YY, NOW, CRM & EBIX

Leveraged Index ETFs: Waiting for new trigger.

The Early Warning Alert Service has hit all seven major market trading points this year. See this brief update video for more details: Early Warning Alerts Update Video or at https://youtu.be/aVE9zqbG4MQ

If simplifying your life by trading along with us using the index ETF is of interest you can get the full background video at: https://activetrendtrading.com/etf-early-warning-alerts-video/

Mike’s Macro Market Musings: Topic: FANG, or deFANGed?

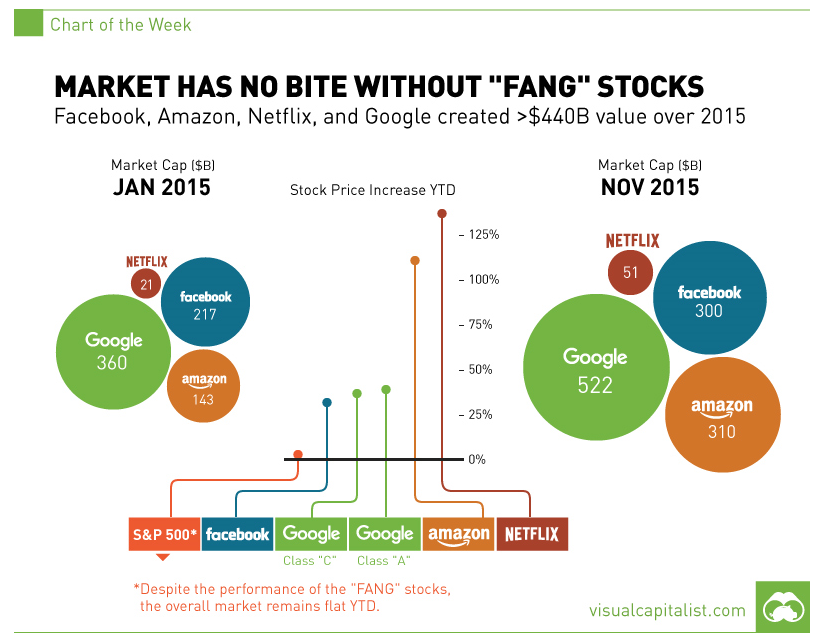

Dennis and I have commented at length recently about the narrowing breadth of the overall market and how the rally in the cap weighted indices such as Nasdaq and the S&P 500 the past several weeks has been driven by a relatively small handful of current large cap market darlings while much of the market has failed to participate. In fact, any positive return in the cap weighted indexes for the calendar year 2015 can be largely attributed to the appreciation of just four stocks denoted by the acronym FANG – Facebook, Amazon, Netflix, Google. We most certainly are not alone in this observation, neither of us pretends to be so prescient. Much of the following information comes from other sources, primarily a website founded by David Stockman. For those of us of a certain advanced age, you may remember David Stockman as a sort of wonder boy of the Reagan administration in the 1980’s – the youngest ever director of the OMB. After a few years of service in that administration, he went on to make his mark and fortune in the private equity industry. As a former insider of both Washington and Wall Street, he knows how things work, and why they sometimes don’t, and he is apparently at a place in his life where he is unafraid to “poke the bear”. Personally, I find the articles on his website a useful source of good information even while sometimes needing to discount the contrarian editorial bias. Where appropriate, quotation marks are used to indicate direct transfer of remarks from Stockman’s article. For those who would like to read the article in full, the website is http://davidstockmanscontracorner.com/when-wall-street-gets-defanged-look-out-below/. Also, for considerations of time references, the article from which the quotes are obtained was published the weekend prior to Thanksgiving (the same weekend I am writing this), so time references come from the week preceding Thanksgiving.

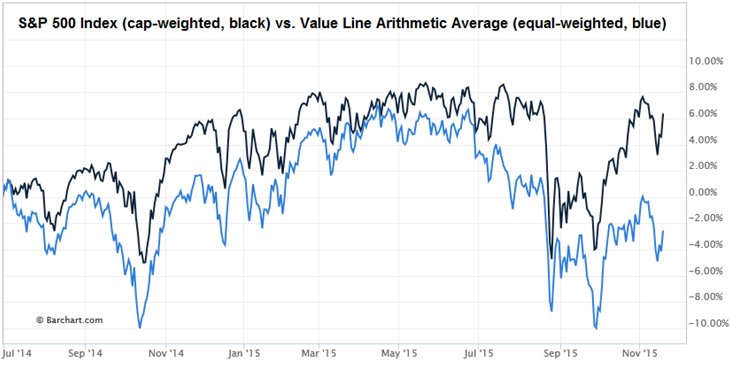

The chart below shows the relative performance of the capitalization-weighted S&P 500 Index (black) and the Value Line Index (blue), an equal-weighted arithmetic index of 1700 of the best-known companies in the stock market. The performance gap between these two indices since mid-2014 has been about 9%. The same type of visual comparison can be replicated by overlaying a similar chart of the S&P 500 with one of the NYSE Composite Index and/or the Russell 2000 index, both of which are similarly equal weighted indexes of thousands of individual stocks. It is quite clear that the performance of equal weighted indexes this past year does not match the performance of cap weighted indexes unduly influenced by FANG and perhaps a few others.

“The market has narrowed down to essentially four explosively rising stocks—–the FANG quartet of Facebook, Amazon, Netflix and Google—–which are sucking up all the oxygen left in the casino.

At the turn of the year, the FANG stocks had a combined market cap of $740 billion and combined 2014 earnings of $17.5 billion. So a valuation multiple of 42X might not seem outlandish for this team of race horses, but what has happened since then surely is. At this week’s close, the FANG stocks were valued at just under $1.2 trillion, meaning they have gained $450 billion of market cap or 60% during the last 11 months——even as their combined earnings for the September LTM period were up by only 13%.”

“An old Wall Street adage holds that market tops are a process, not an event. A peak under the hood of the S&P 500 index, in fact, reveals exactly that. On the day after Christmas last December the total market cap of the S&P 500 excluding the FANG stocks was$17.70 trillion. By contrast, it closed at $17.26 trillion on Friday, reflecting a 2.5% or nearly half trillion dollar loss of value.”

Speaking of valuations, notably those based on metrics such as earnings and revenues, as the cap weighted indexes flirt with their all time highs they are becoming even more expensive than they already were due to reported declines in revenues and earnings for the S&P 500 as a whole. And, as we all should know, eventually valuations not only revert to their longer term averages, they have a tendency to overshoot and not only mean revert but also mean invert. “Reported EPS for the S&P 500 during the LTM ended in September was $94 per share or 11% below the $106 per share reported a year ago.”

Stockman draws parallels between the current FANG stocks relative to the overall market and a similar scenario depicted at the peak of the dot.com boom in early 2000 involving the stocks of MSFT, INTC, CSCO, and DELL, and even similar scenarios seen in hindsight at other historical notable market tops. The similarities are interesting, at least to me, and possibly predictive, even if not immediately actionable.

“But let’s see. It’s more like the same old delusion that trees grow to the sky. At its peak in late March 2000, for example, Cisco was valued at $540 billion, representing a $340 billion or 170% gain from prior year.

Since it had earned $2.6 billion in the most recent 12 month period, its lofty market cap represented a valuation multiple of 210X. And Cisco was no rocket ship start-up at the point, either, having been public for a decade and posting $15 billion of revenue during the prior year. Nevertheless, the bullish chorus at the time claimed that Cisco was the monster of the midway when it came to networking gear for the explosively growing internet, and that no one should be troubled by its absurdly high PE multiple.

The same story was told about the other three members of the group. During the previous 24 months, Microsoft’s market cap had exploded from $200 billion to $550 billion, where it traded at 62X reported earnings. In even less time, Intel’s market cap had soared from $200 billion to $440 billion, where it traded at 76X. Dell’s market cap had nearly tripled during this period, and it was trading at 70X.

Altogether, the Four Horseman had levitated the stock market by the stunning sum of $800 billion in the approximate 12 months before the 2000 peak. That’s right. In a manner not dissimilar to the FANG quartet during the past year, the Four Horseman’s market cap had soared from $850 billion, where it was already generously valued, to $1.65 trillion or by 94% at the time of the bubble peak. There was absolutely no reason for this market cap explosion except that in the final phases of the technology and dotcom bull market speculators had piled onto the last mono trains leaving the station. But it was a short and unpleasant ride. By September of 2002, the combined market cap of the Four Horseman had crashed to just $450 billion. Exactly $1.0 trillion of bottled air had come rushing out of the casino.

Needless to say, the absurdly inflated values of the Four Horseman in the spring of 2000 looked exactly like the FANG quartet today. Thus, Facebook reported $2.8 billion of net income in the most recent period, thereby weighing in with a 107X PE multiple. Likewise, Netflix currently trades at 307X its LTM earnings and Amazon at 950X. Even Google, which has now smacked into the law of large numbers with revenue growth of just 13% in the last year, is valued at 32X.”

“So here’s the thing. The Four Horseman were great companies that have continued to grow and thrive ever since the dotcom meltdown. But their peak valuations were never remotely justified by any plausible earnings growth scenario. In this regard, Cisco is the poster child for this disconnect. During the last 15 years its revenues have grown from $15 billion to nearly $50 billion, and its net income has more than tripled to nearly $10 billion per year. Yet it’s market cap today at $140 billion is just 25% of its dotcom bubble peak. In short, its market cap was driven to the absurd height recorded in March 2000 by the final spasm of a bull market, when the punters jumped on the last mono trains out of the station”

“This time is surely no different. The FANG quartet may live on to dominate their respective spheres for years or even decades to come. But their absurdly inflated valuations will soon be deFANGed.

When that happens, look out below.”

Stockman’s conclusions are his own and seem to be based on logic, reason, and historical precedent, and while he is not alone in his convictions, there is certainly no universal agreement with them among many of the talking heads. As always, price action is king, and price action in the cap weighted indexes certainly has not yet proven his thesis. Food for thought, though, I think, if not for actual physical digestion.

Best wishes to all of you for a wonderful Thanksgiving and a happy holiday season, whichever holiday you choose to celebrate!! Hoping that your trading this year has been profitable enough to drive our national GDP higher via your holiday spending.

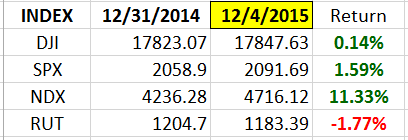

General Market Observation: Last week was a very interesting week for the Tracking Index. All three sold off hard on Wednesday and Thursday and then rebounded on Friday. It is interesting to note and in line with Mike’s article—the weighted indexes (SPX & NDX) rebounded better than the non-weighted RUT. Is there a clue in this action or just a reconfirmation of underlying weakness that may eventually serve as the “Iceberg” for the Titanic? We shall see.

With a high probability of a rate hike by the Fed the markets may rally hard on the expected action and then pullback after the news is out. Each of the indexes is operating within a well-defined trading range with a slight upward bias. Until the Fed reports out the week of December 13th the Indexes may be prone to story related volatile action. If one trades any of the related ETFs look for horizontal support or resistance for planning trades.

SPX: Preferred ETF’s: SPY, UPRO and SPXL

NDX: Preferred ETF’s: QQQ and TQQQ

RUT: Preferred ETF’s: IWM and TNA

The Early Warning Alert Service has hit all seven major market trading point this year. See the updated video at: https://activetrendtrading.com/early-warning-alerts-2/

If simplifying your life by trading along with us using the index ETF is of interest you can get the full background video at: https://activetrendtrading.com/etf-early-warning-alerts-video/

The How to Make Money Trading Stock Show—Free Webinar every Friday at 10 a.m. PDT. This weekly live and recorded webinar helped traders find great stocks and ETF’s to trade with excellent timing and helped them stay out of the market during times of weakness.

The “How to Make Money Trading Stocks” Show Dec 11th

Register Here: https://attendee.gotowebinar.com/register/6593811185251424258

To get notifications of the newly recorded and posted How to Make Money Trading Stocks every week subscribe at the Market Tech Talk Channel: https://www.youtube.com/channel/UCLK-GdCSCGTo5IN2hvuDP0w

The Active Trend Trader Referral Affiliate Program is ready. For more information or to become an Affiliate please register here: https://activetrendtrading.com/affiliates-sign-up-and-login/

_________________________

Index Returns YTD 2015

ATTS Returns for 2015 through Dec 4, 2015

50% Invested

Margin Account = +13.7% (Includes profit in open positions)

Early Warning Alerts = 10.8% Partial Positions; 19.4% Full Positions

Active Trend Trading’s Yearly Objectives:

- Yearly Return of 40%

- 60% Winning Trades

- Early Warning Alert Target Yearly Return = 15% or better

For a complete view of specific trades closed visit the website at: https://activetrendtrading.com/current-positions/

Updated first full week of each month.

___________________________________________________________

For our all Active Trend Trading Members here’s how we utilize our trading capital

Trading Capital Setup and Position Sizing: Every year we start the year off trading a $100K margin account split up into the three strategies used with the Active Trend Trading System.

- Each trader must define their own trading capital in order to properly size trade positions to meet their own risk tolerance level!

- Strategy I: Capital Growth—70% of capital which equates to $140K at full margin. This strategy trades IBD Quality Growth Stocks and Index ETFs. Growth Target 40% per year.

- Strategy II: Short Term Income or Cash Flow—10% of capital or $10K. This strategy focuses on trading options on stocks and ETF’s identified in Strategy I. The $10K will be divided into $2K units per trade.

- Strategy III: Combination of Growth and Income—20% of capital or $20K. This strategy will use LEAPS options as a foundation to sell weekly option positions with the intent of covering cost of long LEAPS plus growth and income.

- The $70K Strategy I portion of the trade account is split between up to 4 stocks and potentially a leveraged Index ETF. Actual number of shares will vary of course depending on price of the entity traded and amount of margin available. We have found that limiting open positions to only 5 entities greatly reduces the trade management time requirements for members.

- Naked Puts or short term options strategies will be used occasionally for Income Generating Positions

- None of the trade setups are recommendations to trade only notification of planned trades from set ups using the Active Trend Trading System. Each trader is responsible for establishing their own appropriate risk level if they decide to parallel trade.

- The Active Trend Trading System objective is to provide a clear and simple system designed for members who work full time.

Outs & Ins: BBCN makes its debut on this week’s IBD 50 list and it’s extended. The Running List has now grown to 205 stocks for the year.

I have begun analyzing the first IBD 50 list of 2015 and as I have each list since 2007. Again the first IBD 50 list of the years was where the “big fish” could be found with ample trading opportunities. One thing I measure every year is the price range from the low to the high of the year for the IBD 50 stocks compared to the S&P. This year from low to high the S&P demonstrated a range of 13.36%. This is a good move but of the 50 stocks on the IBD list, 46 of the stocks moved more. The average move of 92% of the IBD 50 stocks was over 46%.

After analyzing the list for the past 9 years with similar results it continues to confirm that trading stocks from the IBD 50 with the right system will significantly outperform the Indexes!

Share Your Success: Many of you have sent me notes regarding the success you are having with the Active Trend Trading System. Please send your stories to me at dww@activetrendtrading.com or leave a post on the website. Thanks.