Good Day Traders,

Overview & Highlights: This weekend’s edition features a follow-up article by Mike Trager. Mike’s topic covers the new housing bubble, the Fed’s credibility and how this all may be shaping up into the “mother” of all Bear Markets!

The Website performance page will be updated the first full week of every month. Additionally a new video updating the performance to date of the Early Warning Alert System was recorded and is available at: https://activetrendtrading.com/early-warning-alerts-2/

Webinars: At Active Trend Trading we offer two webinars per week to provide training plus trade and market updates. See the schedule below for the next webinars.

How to Make Money Trading Stocks on December 18th

Register Here: https://attendee.gotowebinar.com/register/6170324386318180609

Next Training Webinar: Tuesday, Dec 15th

For Premium Members our Wednesday evening training is developing some fantastic traders!

Mid-Week Market Sanity Check Topic: Part 2: Wealth Building by Portfolio

_____________________________________________________

Managing Existing Trades: The Active Trend Trading System Strategy 1 worked well this week getting us out of trades that were not working well and keeping us in trades that are still working. The system pushed us into an increased capital position as the markets weakened, thus providing the cash when it’s time to buy for the next upside move.

Strategy I: Currently 3 open trades. Hard Stops hit on CRM and AKRX with the market sell off on 12/11.

Trade 1: Entered CBM on a pullback to the 8 day EMA on 11/19. Hard Stop has been moved to breakeven or 49.40. Sold ½ the position when T1 = 54.34 was triggered on 11/25. On 12/9 entered another 175 shares at 51.76. Closed 175 shares at 54.30 for a profit of $857.50

Current position up: 1.5%

Trade 2: Entered NOW at 86.55 today on a bounce from the 8 day EMA on 11/30. T1 = 10% above entry at 95.21 and the Hard Stop is at 83.09.

Current position down: -3.6%

Trade 3: Entered HAWK at 47.10 on 12/3 on a bounce from the 8 day EMA. T1 = 10% above entry at 51.81 and the Hard Stop is at 45.22.

Current position down: -0.6%

Trade 4: Entered CRM at 35.32 on 12/10 on a bounce from the 8 day EMA. T1 = 10% above entry at 88.72 and the Hard Stop is at 77.43—Stop Hit on 12/11 selling all shares at 77.41

Position Closed 4.1% Loss

Trade 5: Entered AKRX at 80.66 on 12/8 on a bounce from the 8 day EMA. T1 = 10% above entry at 38.85 and the Hard Stop is at 33.91—Stop Hit on 12/11 selling all shares at 33.96

Position Closed 3.9% Loss

____________________

Strategy II: No Open Trades

____________________

Wealth & Income Generation Strategy III Trades: If the value of the underlying Long Options plus the premium cleared from selling weekly options approaches 100% on any trade I will close the position and start a new position. With the IWM trade below because there is only 9 weeks until the long positions expire, I will look to close the total position if return approaches between 30-50%.

Trade 1: Long IWM Jan16 127C & 127P – Closed this first demonstration trade of a profit of 3% equaling $299 in profit.

Trade 2: Long TSLA Jan17 250C & Long Jan17 220P – One position this week stopped for loss of $180

Several members have asked about this strategy and a more detailed explanation is available at: https://activetrendtrading.com/wealth-and-income-strategy/ .

I posted a video about how to choose the weekly options to short for this strategy. It can be viewed at: https://activetrendtrading.com/videos/

Additionally some of these trade may be selling weekly puts on up trending stocks. If you are interested in parallel trading this strategy register at this link: http://forms.aweber.com/form/99/1278533099.htm

_________________________________________________

Pre-Earnings Trade: Will wait for Q4 earnings that start in 2016.

_________________________________________________

Potential Set Ups for this week: I am not in a hurry to make long term trades until the Fed meeting and reports out next Wednesday. I’ll be flying to Arkansas to help my mom move into here new assisted living complex when the Fed reports out. Hopefully opinions and initial reactions to the decision will start working out Thursday and Friday. I’m will be looking for 2 stocks to add to the portfolio on Strategy I moving forward. With the market correcting look for the strongest stocks that hold up while the market shows weakness.

Upside: CBM & HAWK

Downside: JAZZ, V, NFLX & TSO

On the Radar: TSLA, HA, IMAX, LNKD, PANW, YY & AMBA

Leveraged Index ETFs: Standby Alert Issued, No Buy Signal Yet.

The Early Warning Alert Service has hit all seven major market trading points this year. See this brief update video for more details: Early Warning Alerts Update Video or at https://youtu.be/aVE9zqbG4MQ

If simplifying your life by trading along with us using the index ETF is of interest you can get the full background video at: https://activetrendtrading.com/etf-early-warning-alerts-video/

Mike’s Macro Market Musings: Topic: Housing Bubble 2.0; Central Bank Credibility, R.I.P.

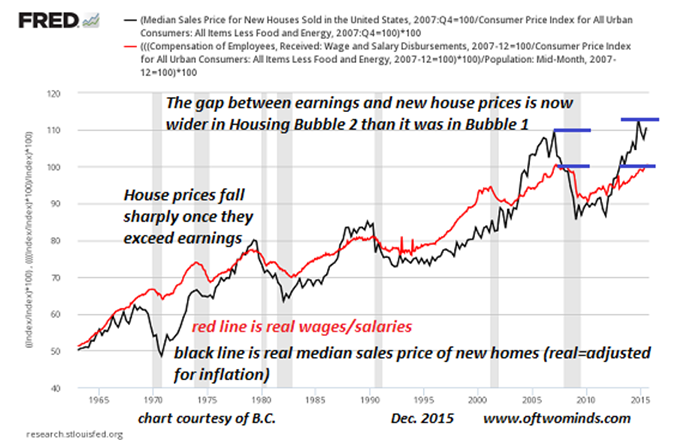

There are some main stream media talking heads and central bank officials (yes, that means you, Ms. Yellen) who, at least publicly, are unwilling or unable to admit to or concede at least the possibility of the bubbles in the financial markets that have resulted from seven years of zero interest rate policy (ZIRP) in the U.S. and many trillions of dollars and other currencies that have been created out of thin air during that time. One market that has especially benefitted from all of this has been the real estate market both here and abroad; specifically, the residential housing market. In fact, here in the U.S., the bubble in residential housing is now possibly greater than it was in 2005-2006 before it collapsed, taking both domestic and global equity markets down with it. That is, a residential housing bubble based on at least one metric which compares inflation adjusted (i.e. real) median housing prices for new houses to inflation adjusted median household income, possibly better referred to for shorthand discussion purposes as “affordability”.

The following chart has been produced by the research department of the St. Louis branch of the Federal Reserve:

I believe this chart speaks for itself. The gray vertical bands in the chart denote periods of economic recession in the U.S. which also correspond with significant declines in U.S. equity markets (surprise, surprise). Over the past 50+ years, when the percentage increase in real new home prices outpaces the percentage increase in median household income, at some point a mean reversion or even an inversion has occurred such that the increase in income matches or even outpaces the increase in home prices. Peaks in home prices and extremes in the price/income relationship often precede periods of recession and major corrections or even bear markets in U.S. equities. Note that this gap is currently even wider than it was at the peak of the housing bubble in 2005-2006 and the widest it has ever been going back more than 50 years. Will things turn out differently this time than it has in the past? Doesn’t seem likely, just seems to be a matter of when and the ultimate magnitude of the reversion. And when it happens as it has before, the talking heads, which include Ms. Yellen, will claim, as they have before, there was no way to see it coming and bubbles are only evident in hindsight. Right.

Speaking of which, this provides a nice segue into a brief discourse on the death of credibility previously enjoyed by global central banks, of which the U.S. Federal Reserve is the 800 pound gorilla. This is being written on December 5, 2015, after a week of significant ups and downs in global equity markets. This was the week that Mario Draghi, head of the European Central Bank (ECB), the European equivalent of Janet Yellen, current chairwoman of the U.S. Federal Reserve Bank, publicly announced planned changes to the current QE program in Europe which was implemented earlier this year and is not yet quite producing the hoped for results in the European economic statistics. His announcement disappointed European and U.S. equity markets which were hoping for more of an expansion of the ECB QE program than he was indicating, resulting in a significant down day in the equity markets on 12/3/15. Can you possibly guess what happened afterwards?

On 12/4/15, the very next day, Draghi gave a speech in New York indicating that he would now give the markets what they wanted, more QE, even stating that there was no limit to how much money the ECB would print and for how long, leaving the whole consideration open ended. The markets responded to this as might be expected with a huge up day, completely erasing the losses of the previous day and then some. The motivation of the heads of global central banks can no longer be in doubt. Despite proclamations of charters and mandates to promote price stability and act as lenders of last resort to backstop banks and economies during times of financial distress, and despite Janet Yellen’s public statements early in 2015 that she had no intention of babysitting the equity markets through corrections, their actions directly and consistently contradict their statements.

The following video clip from CNBC is taken from a Q&A session with Draghi immediately after his speech of 12/4/15 and runs for about 90 seconds, the pertinent question and answer occurs at around the 50 and 60 second mark, and the interviewer is Mervyn King, former head of England’s central bank – http://video.cnbc.com/gallery/?video=3000463140

The following quote just about sums it up – “the following exchange between Mervyn King, in which the former BOE chief asked “was today’s speech deliberately designed to try offset some of the reaction yesterday?” to which Draghi had a response that shocked every central bank watcher in its brutal honesty that all that matters to the ECB at this point is the market:

“Not really… well, of course.” And there it is: at the end of the day, all modern monetary policy devolves to is offsetting a “negative market reaction”. The timing of the initiation of QE3 in September, 2012, by Ben Bernanke after a good sized correction in U.S. equity indexes seemingly offers further proof of this conviction.

And, I believe it is readily apparent that Draghi and Yellen and others know very well that their words, perhaps even more so than their actions, will have their intended effect, and they conduct themselves accordingly. In fact, in late 2012, the New York Federal Reserve branch released an internal study done to measure the effect of the policies and statements of the Federal Reserve over time on financial markets. While I do not know what kind of methodology was utilized to make this determination, the Fed’s own conclusion was that U.S. equity indexes were at that time 50% higher than they would otherwise be were it not for Fed policies and statements.

For those of you who have become involved with the financial markets in just the past few years, make no assumption that the markets as you have experienced them so far are behaving in a historically consistent manner. The short term micro management of the markets by the central banks, affirmed here by the head of one of the major global central banks, has literally no historical precedent. The unelected academicians responsible for this seem to have decided to use the markets as a policy tool with preset goals or targets for nominal equity prices to support what they believe should be the goals for their monetary policies. Any deviations (i.e. shortcomings) from these price targets are not to be tolerated for long and have been met with corresponding additions to already historically unprecedented easy money policies. At least for now, and for longer than I ever believed possible, the equity markets are no longer allowed to freely reflect the true economic and valuation fundamentals upon which they have historically been built. The resultant distortions are evident in any number of metrics one might choose to examine. In their more candid moments, they have at least acknowledged that for the past several years all of this has been a big experiment which, with no precedent, has no known outcome. In my humble opinion, the irresponsibility exhibited by the heads of the global central banks via these manipulations with no apparent regard for the potential resolution of the distortions they have created and consequent effects on the lives of literally billions of people, knowing that they (the central bank leaders, that is) will not be held accountable, is reprehensible, the most polite adjective I can conjure up at this moment.

Credibility? Can’t see it coming? Please. I could go on, but space limitations here won’t allow for that. Watch the charts, act accordingly. Enjoy the holidays!

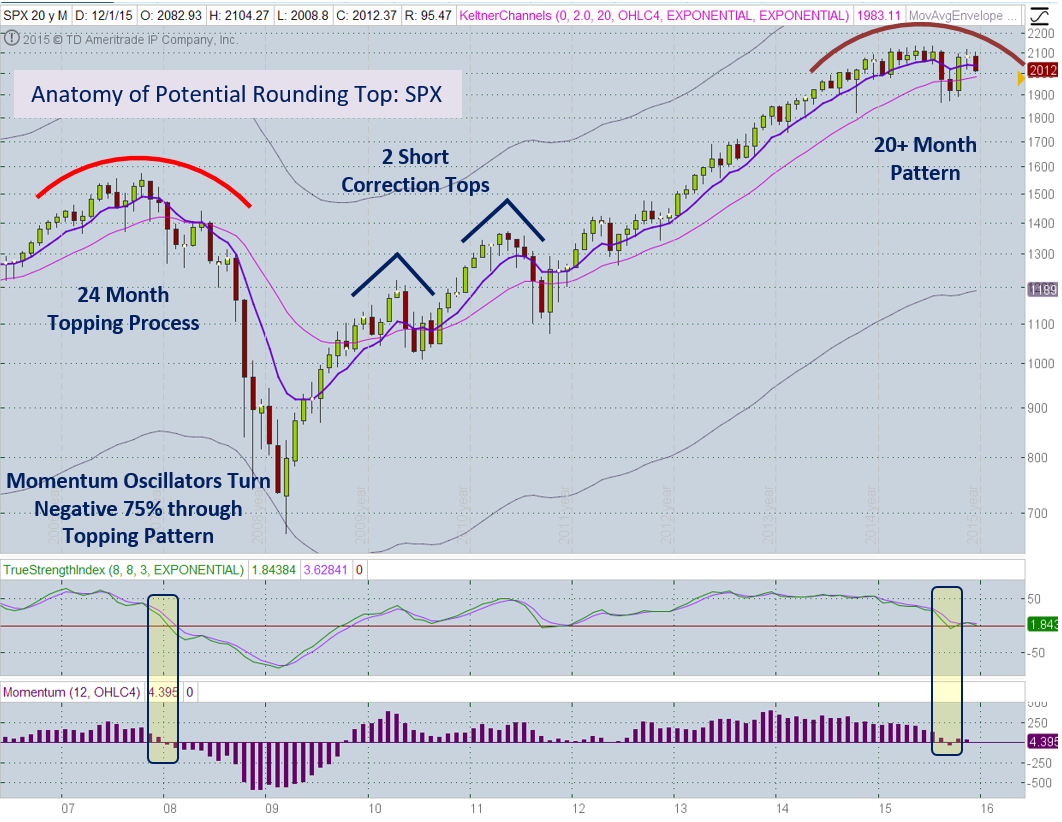

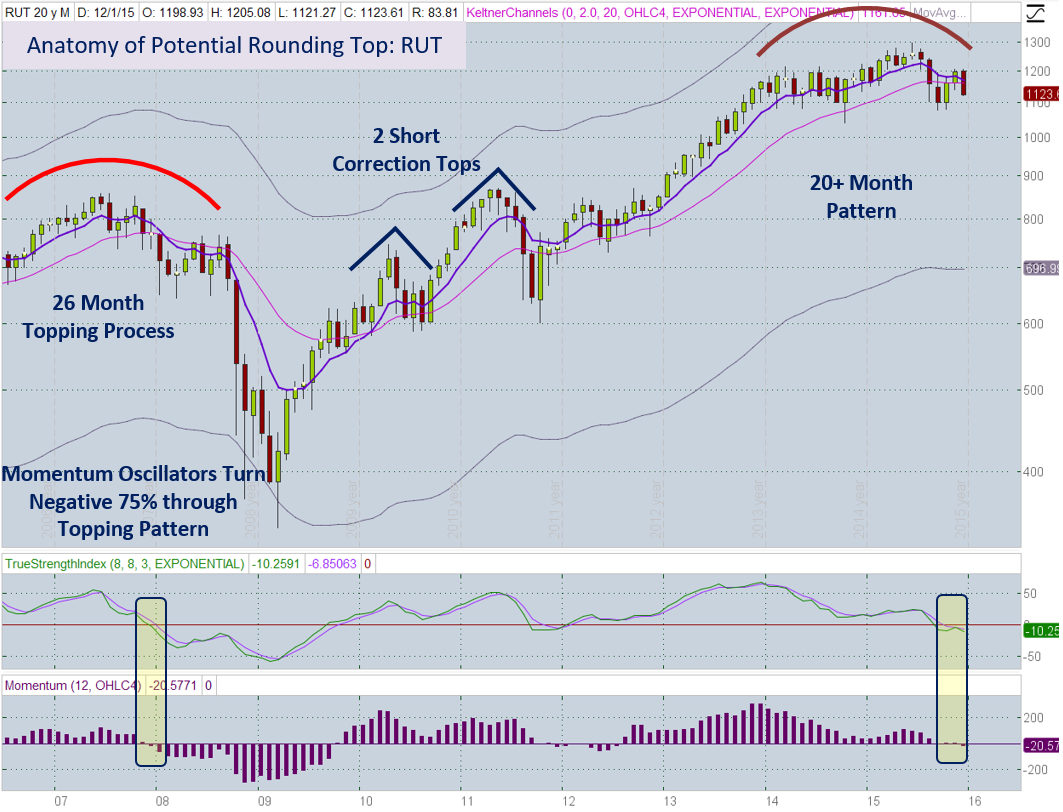

General Market Observation: Fridays’ price action on all market’s including overseas markets topped off a down week where some of the underlying market weakness may have become more apparent. Could the under-participation and deteriorating foundational support for the valuations finally be building to a crescendo that will set up next Bear Market? Friday’s action took out strong support on both the SPX and RUT. The NDX held above strong support at 4500 but did slice through and finish below the 50 day EMA. I won’t venture to guess why prices were so weak leading up to next weeks Fed Meeting, but next week could provide fireworks regardless of what action the Fed decides to take. With the Fed meeting looming I plan on keeping my powder dry until after the Fed announces on December 16th.

While I try to be neither overly optimistic nor pessimistic about the potential direction of the market, I spent time this weekend looking at the monthly charts of the Tracking Indexes. The monthly charts of both the S&P and Russell stood out because price action over the past 13 months or more looks to be putting in a slow rounding top. Slow rounding tops tend to lead to significant corrections. On the charts below look at current monthly conditions and compare the similarities with the 2007-2008 time frame. Some of the similarities include a long term resistance zone that stymies upside progress for months. The 2100 level on the SPX has acted as resistance for 13 months.

Next the long term negative divergence of Momentum. Both the S&P and RUT show monthly momentum that became negatively divergent in January 2014. Lastly both TSI and Momentum oscillators moving below the “zero” line. Does this mean the market will crash on Monday? Probably not, but when there is a convergence of clues we need to pay attention. These three clues are pretty strong clue that a more significant correction is in the not too distant future. How nasty will it be? At this point who knows! Regardless there will be opportunities during rebounds just like 2008. After the Russell finally turned over there was a respite where a 16% rally took place over a 7 month rally. If the market does choose 2016 to roll over could lead to a very interesting election year here in the States.

SPX: Preferred ETF’s: SPY, UPRO and SPXL

NDX: Preferred ETF’s: QQQ and TQQQ

RUT: Preferred ETF’s: IWM and TNA

The Early Warning Alert Service has hit all seven major market trading point this year. See the updated video at: https://activetrendtrading.com/early-warning-alerts-2/

If simplifying your life by trading along with us using the index ETF is of interest you can get the full background video at: https://activetrendtrading.com/etf-early-warning-alerts-video/

The How to Make Money Trading Stock Show—Free Webinar every Friday at 10 a.m. PDT. This weekly live and recorded webinar helped traders find great stocks and ETF’s to trade with excellent timing and helped them stay out of the market during times of weakness.

The “How to Make Money Trading Stocks” Show Dec 18th

Register Here: https://attendee.gotowebinar.com/register/6170324386318180609

To get notifications of the newly recorded and posted How to Make Money Trading Stocks every week subscribe at the Market Tech Talk Channel: https://www.youtube.com/channel/UCLK-GdCSCGTo5IN2hvuDP0w

- The Active Trend Trader Referral Affiliate Program is ready. For more information or to become an Affiliate please register here: https://activetrendtrading.com/affiliates-sign-up-and-login/

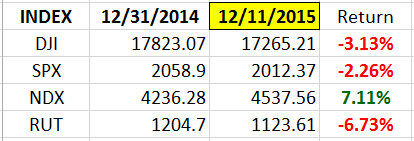

Index Returns YTD 2015

ATTS Returns for 2015 through Dec 11, 2015

51% Invested

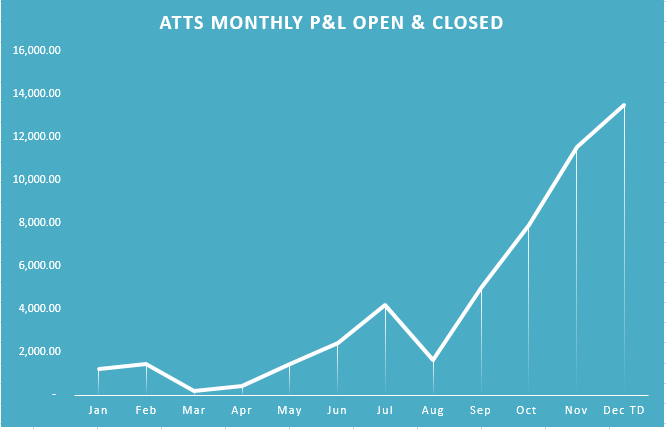

Margin Account = +13.5% (Includes profit in open positions). See chart below for monthly tracking.

Early Warning Alerts = 10.8% Partial Positions; 19.4% Full Positions

Active Trend Trading’s Yearly Objectives:

Yearly Return of 40%

60% Winning Trades

- Early Warning Alert Target Yearly Return = 15% or better

For a complete view of specific trades closed visit the website at: https://activetrendtrading.com/current-positions/

Updated first full week of each month.

___________________________________________________________

For our all Active Trend Trading Members here’s how we utilize our trading capital

Trading Capital Setup and Position Sizing: Every year we start the year off trading a $100K margin account split up into the three strategies used with the Active Trend Trading System.

- Each trader must define their own trading capital in order to properly size trade positions to meet their own risk tolerance level

- Strategy I: Capital Growth—70% of capital which equates to $140K at full margin. This strategy trades IBD Quality Growth Stocks and Index ETFs. Growth Target 40% per year.

- Strategy II: Short Term Income or Cash Flow—10% of capital or $10K. This strategy focuses on trading options on stocks and ETF’s identified in Strategy I. The $10K will be divided into $2K units per trade.

- Strategy III: Combination of Growth and Income—20% of capital or $20K. This strategy will use LEAPS options as a foundation to sell weekly option positions with the intent of covering cost of long LEAPS plus growth and income.

- The $70K Strategy I portion of the trade account is split between up to 5 stocks and potentially a leveraged Index ETF. Actual number of shares will vary of course depending on price of the entity traded and amount of margin available. We have found that limiting open positions to only 5 entities greatly reduces the trade management time requirements for members.

- Naked Puts or short term options strategies will be used occasionally for Income Generating Positions

- None of the trade setups are recommendations to trade only notification of planned trades from set ups using the Active Trend Trading System. Each trader is responsible for establishing their own appropriate risk level if they decide to parallel trade.

- The Active Trend Trading System objective is to provide a clear and simple system designed for members who work full time.

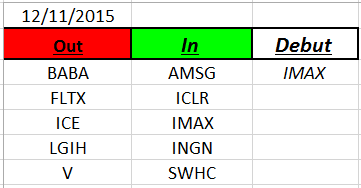

Outs & Ins: IMAX makes its debut on the IBD 50 list. IMAX has been a member of the Leaderboard for a couple of weeks, so having it also show up on this list is not a surprise. Unlike many stocks that debut to this elite list IMAX is actually not extended! It is in the handle portion of a C&H pattern with a breakout buy point of 39.97. If the market continues to weaken the C&H pattern may fail. Momentum and TSI on the weekly chart appears to support more downside.

To date in 2015 207 stocks have appeared on the IBD 50. An interesting note: 24 of the stocks on the IBD list are now below their 8 week EMA which is not a sign of a strong uptrend!

Share Your Success: Many of you have sent me notes regarding the success you are having with the Active Trend Trading System. Please send your stories to me at dww@activetrendtrading.com or leave a post on the website. Thanks.