Good Day Traders,

Overview & Highlights: Happy Valentines! Great article by Mike Trager in this edition. Mike hits the high points of Volatility and some of the current biases that may be present in the current market environment. Additionally, I am watching the price action on the Indexes to see if the action follows the historic seasonality which predicts a drop the indexes between now and April. We shall see!

I hope all members have seen some of the live Facebook broadcast. If you want notification of when these live market updates take place please follow Active Trend Trading at: https://www.facebook.com/ActiveTrendTrading/

Upcoming Webinars: At Active Trend Trading we offer three webinars per week to provide training plus trade and market updates. See the schedule below for the next webinars.

The How to Make Money Trading Stock Show—Free Webinar every Friday at 11:00 a.m. PDT. This weekly live webinar helped traders find great stocks and ETF’s to trade with excellent timing and helped them stay out of the market during times of weakness. With guest from around the world you get a great Global perspective.

The How to Make Money Trading Stock Show—Free Webinar every Friday at 11:00 a.m. PDT. This weekly live and recorded webinar helped traders find great stocks and ETF’s to trade with excellent timing and helped them stay out of the market during times of weakness.

How to Make Money Trading Stocks on Friday, Feb 17th

Register now for the next live webinar at the link below:

Register Here: https://attendee.gotowebinar.com/register/8627485493774470402

Time 11:00 a.m. PDT

Next Training Webinar: Feb 15th

For Premium Members, our Wednesday evening training is developing some fantastic traders

Topic: Seasonality tied to the Leveraged ETFs

** Friday’s “Final Hour”: Feb 17th **

Time 12:00 p.m. PDT

For Premium Members, provides trades and set ups during the final hour of weekly trading.

Mike’s Macro Market Musings: V is for Volatility, and How I Learned to Stop Shorting The Markets

Once upon a time, after having been a long-term investor for much of my adult life, I became enthralled and excited with the idea that one could actually generate trading profits as the markets were going down. Having learned to read charts, I then implemented this idea with decidedly mixed results (I will fully acknowledge this is my own fault and the result of a lack of patience and discipline) and have come to the conclusion that while, yes, it is possible to make money on the downside, it is a strategy I no longer care to pursue. I’ve come to this conclusion based on my own admittedly flawed personal experience and also on some study and thought related to the history of the U.S. equity markets.

Since the very beginning of the U.S. public equity markets, there has been an upside bias. Even a casual examination of the charts of market indexes going back well over 100 years, most notably the Dow Jones index (more about the Dow in a paragraph or two), will demonstrate a very prominent long term uptrend with occasional pullbacks along the way. This uptrend is not only a reflection of steady economic and technological progress, but also a result of rules and regulations that have been put into place and practice to prevent or at least mitigate significant corrections. No institution promotes or practices policies specifically designed to drive markets down – never have, never will. While neither a rule or regulation, the survivorship bias of the indexes commonly used to track our equity markets certainly plays a large role in the continuance of this observed very long term uptrend.

What is survivorship bias? Glad you asked. For illustrative purposes I will confine the following discussion to the Dow Jones Industrial Index, an admittedly flawed benchmark for the U.S. equity markets, but the same concept and practice applies to all of the equity market indexes. The Dow is not a static index. The 30 stocks that comprise this index are changed from time to time via substitutions as determined by the discretion of a panel of editors at the Wall Street Journal, and the index is a price weighted index, meaning that higher priced stocks have more influence on the overall index level than do lower priced stocks. Substitutions in the composition of the index can occur for a couple of reasons. One reason is that the stock is no longer available for trading due to mergers and acquisitions or the company is taken private and off of the public markets, or divides into multiple entities. Another reason is that the WSJ editorial panel might deem a substitution appropriate for a variety of considerations. While stock selection is not governed by quantitative rules, a stock typically is added to the index only if the company has an excellent reputation, demonstrates sustained growth and is of interest to a large number of investors. Most recently, in the past 4-5 years, there have been 5 substitutions, a 16-17% turnover in the index composition. Most notably, on 9/20/13, Visa, Nike, and Goldman Sachs were chosen to replace Hewlett Packard, Alcoa, and Bank of America, and in 2015 Apple was substituted for AT&T. In every instance, the nominal price of the new replacement stock was, and continues to be, higher than the price of the previous stock. The “surviving” stocks are higher priced and better performers than the stocks they replaced that didn’t “survive”. Hence the upward longer term influence on the Dow index attributable to survivorship bias.

Much has been made in the media of the recent attainment of the 20,000 price level of the Dow. We now know that survivorship bias has much to do with this. For added perspective, let’s turn to David Rosenberg, a notable and well respected economist and investment strategist often referred to and quoted by the financial media. As noted in a recent article in Barron’s on January 28, 2017, “survivorship bias also has benefited the Dow. Since April 2004, Dave found that, if the eight companies that were replaced in the DJIA had been kept on, the blue chips would have been at just 12,885 now. That date, by the way, is the furthest back he could go to find former Dow companies that are still around. Rosenberg notes that tech stocks now account for a quarter of the Dow, up from 2% at the peak of the dot-com boom in 1999.” (side note – do you think that this has something to do with upside price bias in the Dow index? Just saying)

This is why I am no longer interested in shorting the market indexes. There is a built in upside bias to the indexes that is constantly and continuously reinforced by the powers that be. I just no longer care to fight that particular tape. In the long run, while potentially occasionally profitable, it is a losing battle. Better to trade with the trend. The “powers that be” can print money to offset whatever losses they may incur. I can’t.

V is for Volatility

Markets have been eerily calm. It’s now been 40 trading days since the last move of 1 percent in the S&P 500, and that was an up day. Stocks haven’t had a down day of 1 percent in more than 80 trading days — and that was in early October. Historical stuff.

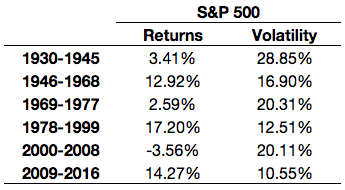

This period of subdued volatility extends beyond the past few months. Volatility in stocks has been below average in the past few years. The annualized volatility of the daily returns on the S&P 500 from 1930 to 2016 is around 19 percent. In 2008, this number shot up well above 40 percent, which was the highest level of volatility we’ve seen since the Great Depression. Volatility continued to be above average in 2009 and 2011. Since then, however, there’s been a severe drop-off every year.

From 2012 to 2016, the average annual volatility was less than 13 percent on the S&P 500, about 30 percent lower than average. And even though it may not feel like it to some investors, this has been an extremely low volatility rally in stocks. We’ve been in a sweet spot of a combination of above average returns and below average volatility.

Investors just need to remember that volatility and performance in stocks can be very cyclical over time. The opposite of the sweet spot that we’re in is lower-than-average returns with higher-than-average volatility. In fact, that’s what investors experienced before this bull market took off in 2009. You can see from the following table that there have been very distinct volatility regimes over time in the stock market:

It shows that periods of poor performance and high volatility tend to be followed by periods of great performance and low volatility. These things don’t run on a set schedule, but it makes sense for investors to understand how markets typically function over the long haul. This shows how the cycle of fear and greed can play tricks on investors over time. When markets become too calm, investors can become complacent. This can lead to overreactions and increased volatility down the line. And when markets become too volatile, it can put investors on edge far too often. This swings the pendulum in the other direction and can lead to decreased volatility. Highly volatile, low-returning markets end in fear, which leads to higher-returning markets with much lower volatility, followed by the eventual greed that starts the cycle again.

Markets move in cycles determined by the cycles of fear and greed of the carbon-based market participants. They have always done so and always will. This time is no different in that respect. Human nature just doesn’t change that quickly. Central banks and other institutions can put policies in place that can change the duration and timing of cycles, but they cannot eliminate them. The markets have enjoyed a period of historically low volatility and above average appreciation over the past several years. Inevitably, at some point, this will change and there will be a period of several years of heightened volatility and sub-par returns. This expectation also ties into the extreme overvaluation of current markets and the expectations of consequential inevitable sub-par market returns to come, as noted in recent postings of this column. The only question at this time continues to be the timing, duration, and magnitude of the coming cyclical turn in both valuations and volatility.

General Market Observation: If symmetry is maintained with thrust between 12/2 and 12/13 price action on the SPX may reach the 2360 zone. This also coincides with a 261.8% extension from the last pullback. It appears that the market is ignoring the hiccups with the new administration as a steady stream of action is underway on taxes and less regulation constraints. A push to the 2360 level is less than 1% away. We shall see if this level serves as adequate resistance to turn back the current uptrend. If the SPX continues to put in higher highs and lows the uptrend will continue. Trade the pullbacks until the uptrend is broken. There is strong support at 2300 the previous breakout level.

The NDX also continues to move to record highs. A similar 261.7% extension sits at 5323 about 1% away from current price levels. Wait for pullback entries. The RUT has moved above the 1392 level and looks ready to push higher but with less momentum than either of the other two Tracking Indexes. If the Indexes go in to a historical pullback look for the Russell to retreat more quickly. This would bring either puts on the IWM or going long the inverse TZA. At this point no reversal triggers have fired.

SPX: Downside Market Short the SPY, SPY Puts or SPXU.

Preferred Long ETF’s: SPY, UPRO and SPXL

NDX: Downside Market Short the QQQ, QQQ Puts or SQQQ.

Preferred Long ETF’s: QQQ and TQQQ

RUT: Downside Market Short the IWM, IWM Puts or TZA.

Preferred Long ETF’s: IWM and TNA

The How to Make Money Trading Stock Show—Free Webinar every Friday at 11:00 a.m. PDT. This weekly live and recorded webinar helped traders find great stocks and ETF’s to trade with excellent timing and helped them stay out of the market during times of weakness.

How to Make Money Trading Stocks on Friday, Feb 17th

Register now for the next live webinar at the link below:

Register Here: https://attendee.gotowebinar.com/register/8627485493774470402

Time 11:00 a.m. PDT

To get notifications of the newly recorded and posted How to Make Money Trading Stocks every week subscribe at the Market Tech Talk Channel: https://www.youtube.com/c/MarketTechTalk

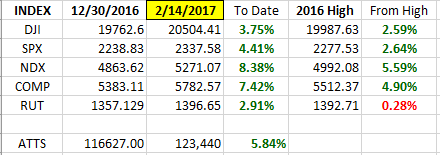

Index Returns 2017 YTD

ATTS Returns for 2017 YTD

Percent invested initial $116.6K account: Strategies I & II invested at 13.76%; Strategy III invested at 26.6%

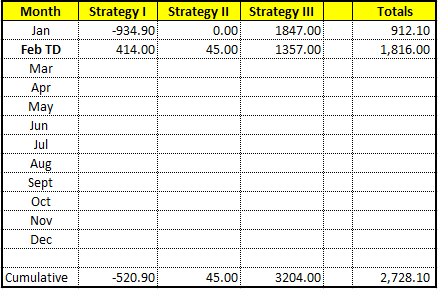

Current Strategy Performance YTD (Closed Trades)

Strategy I: Down -$520.90

Strategy II: Up $45.00

Strategy III: Up $3204.00

Cumulative YTD: 2.34%

Active Trend Trading’s Yearly Objectives:

– Yearly Return of 40%

– 60% Winning Trades

– Early Warning Alert Target Yearly Return = 15% or better

For a complete view of specific trades closed visit the website at: https://activetrendtrading.com/current-positions/

Updated first full week of each month. The next update after first week in March.

Outs & Ins: The IBD 50 only shuffled between stocks on the Running List today. I find it interesting that fewer stocks are popping to the top of the Strength Sort I conduct when the new list comes out. Part of what’s going on is that as members of the list report earnings adjustments are being made to EPS and projected growth. This adjustment has cause fewer stocks to pass all the Fundamental Strength thresholds.

As of today, only IDCC and THO popped to the top. IDCC has earnings on 2-23 BMO and THO reports on 3-6 AMC.

Share Your Success: Many of you have sent me notes regarding the success you are having with the Active Trend Trading System. Please send your stories to me at dww@activetrendtrading.com or leave a post on the website. Thanks.