Good Day Traders,

Overview & Highlights: Today’s Trader’s Report has a great market analysis comparing now with the market rollover in 2008. What are the similarities and differences? Then Mike Trager provides another installment of “Mike’s Macro Market Musings”. Today’s topic provides some very sobering insight into how well the 6th year in the decennial market cycle traditionally performs.

Webinars: At Active Trend Trading we offer two webinars per week to provide training plus trade and market updates. See the schedule below for the next webinars.

How to Make Money Trading Stocks on Friday, Jan 15th

Register Here: https://attendee.gotowebinar.com/register/1285247001330231553

Next Training Webinar: Jan 12th

For Premium Members our Wednesday evening training is developing some fantastic traders!

Mid-Week Market Sanity Check Topic: Enhancing the Compound Effect

Mike’s Macro Market Musings — Topic: Thoughts for 2016; Mind the “E”

“Predictions Are Difficult…Especially When They Are About the Future” – Niels Bohr

Much of my writing of these columns for Dennis is sourced from a variety of reading in which I regularly engage. Due to holiday lethargy, rather than posting my own take on the things I read about, today I will mostly simply copy and paste excerpts from what I consider to be some interesting information and perspective on the coming year in the financial markets. Most of this is taken from an article posted on January 1, 2016, by Lance Roberts, whose commentaries posted on his website I often find informative, logical, and well thought out, if not particularly actionable. For those of you interested in reading the full text, here’s the link: http://realinvestmentadvice.com/2016-market-outlook-forecast-01-01-16/ Keep in mind as you read through this the following ten rules of investing from Bob Farrell, and also keep in mind how these might apply to recent articles in which I have written about valuations, mean reversion, market breadth, etc. For those of you who may not be familiar with him, he helped pioneer the establishment of technical analysis in the financial markets in the late 1950’s. Many of the basic concepts and tenets of technical analysis originated with him. Also, keep in mind that currently the U.S. equity market (i.e. DJIA, S&P 500) has enjoyed the longest period of time EVER without experiencing a correction of 20% or more. Here are the ten rules:

- Markets tend to return to the mean over time

- Excesses in one direction will lead to an opposite excess in the other direction

- There are no new eras — excesses are never permanent

- Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways

- The public buys the most at the top and the least at the bottom

- Fear and greed are stronger than long-term resolve

- Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names

- Bear markets have three stages — sharp down, reflexive rebound and a drawn-out fundamental downtrend

- When all the experts and forecasts agree — something else is going to happen

- Bull markets are more fun than bear markets

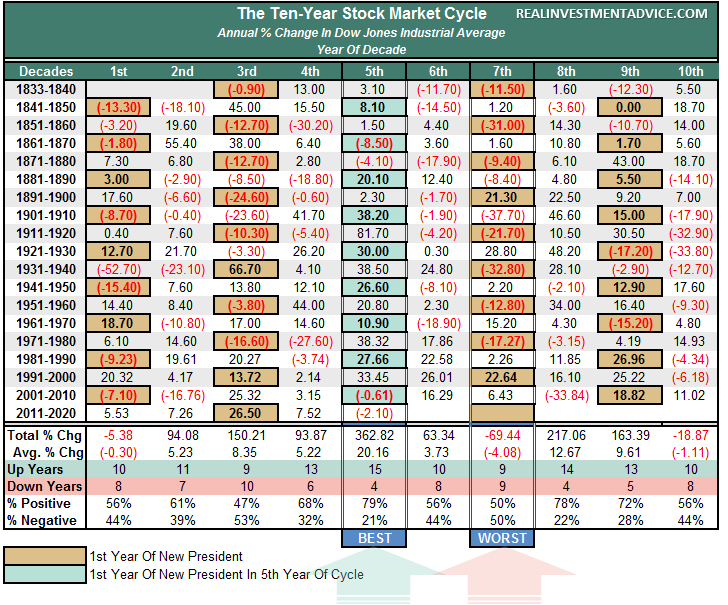

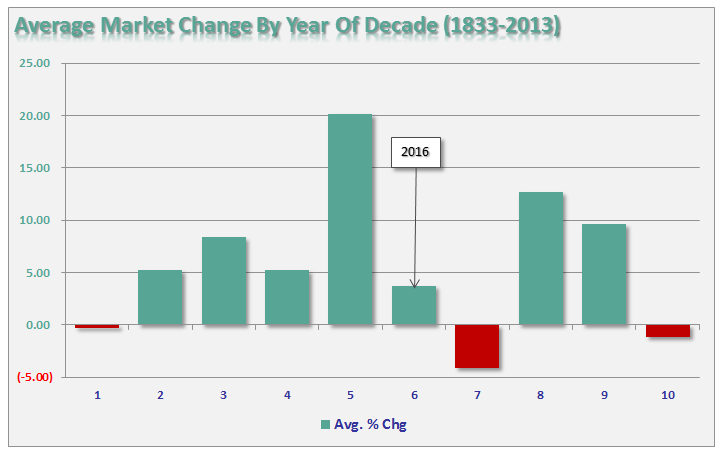

2016 – The Odds of Positive Year Fall Sharply

As we enter into the 6th year of the decade, what do the decennial trends tell us about the probabilities of stock market returns in the coming year?

In reviewing 2015, we find that the 5th year of the decade has been positively biased over its history turning in an average return of 20.16% with positive years outnumber losing ones by 15 to 4. 2015 was one of the rare exceptions with the market dropping 2% for the year.

2016 may also continue to be tough sledding as the odds of a positive return year fall from 79% to 56%. Also, the average rate of return falls to just 3.73% which is far below the average expected by Wall Street analysts (above) of 7.7%.

While statistics say that 2016 leans more heavily towards positive returns – the final outcome will have much to do with a common theme you will see throughout this report today – the economic recovery may be over.

2016 Outlook & Forecast

Each year, as I prepare to write my outlook and forecast, I read many of the mainstream analyst’s predictions to get a gauge on the “consensus.” This year, more so than most, the outlook for 2016 is universally, and to some degree exuberantly, bullish. What comes to mind is Bob Farrell’s Rule #9 which states:

“When everyone agrees…something else is bound to happen.”

As noted above, the “consensus” suggests that 2016 will be a continuation of the last seven years with respect to rising stock markets with estimates the S&P 500 could top 2300 next year. It is also “hoped” that the economy will return to stronger trends of economic growth to finally achieve “escape velocity” which will lead to real improvements in employment and income growth.

Could such really be the case? Honestly, I don’t know. However, the following are my best “guesses” for the coming year, based on the statistical and technical data trends, for the market, interest rates, the dollar, employment and the economy.

S&P 500 Posts a Negative Return Year

If you take a look around Wall Street, it is hard to find anyone that expects a negative year in 2016. However, bull markets do not last forever and with deteriorating earnings, narrow market breadth and declining momentum, there are ample signs that the first half of this particular market cycle is nearing its end.

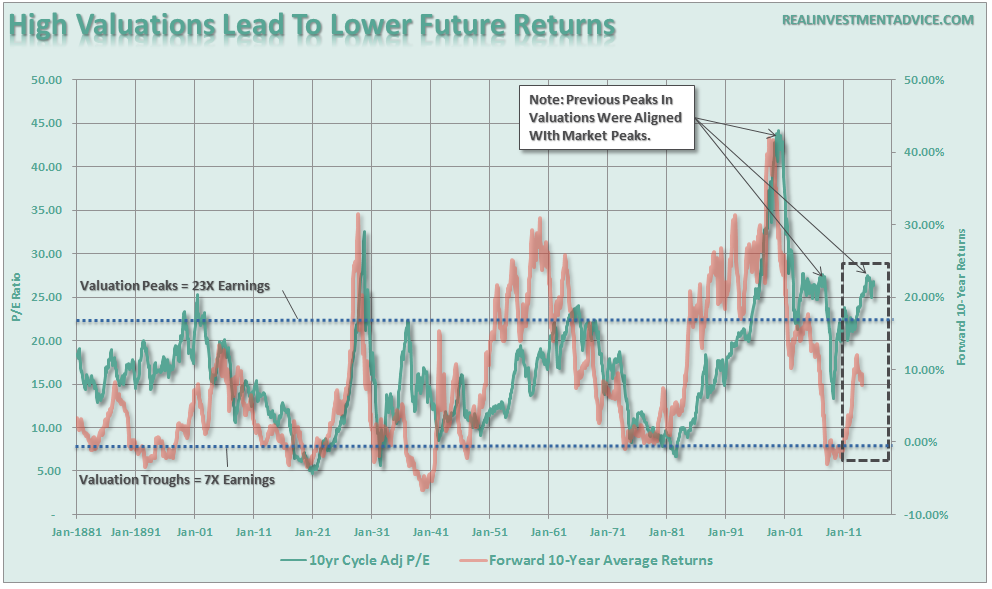

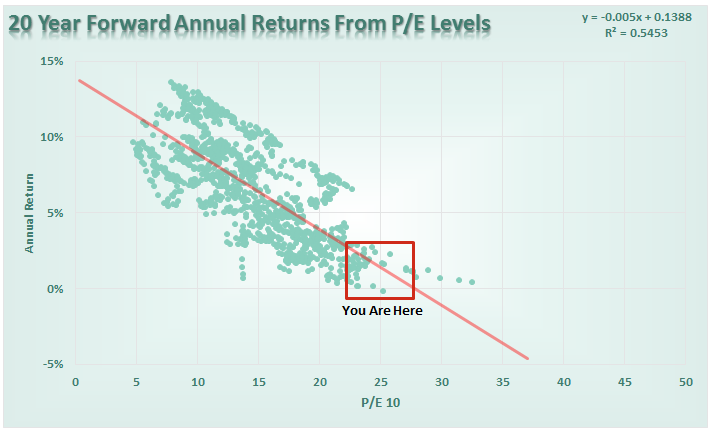

As shown in the two charts below, stocks are expensive by any legitimate measure which suggests that annualized rates of return will be low in the future.

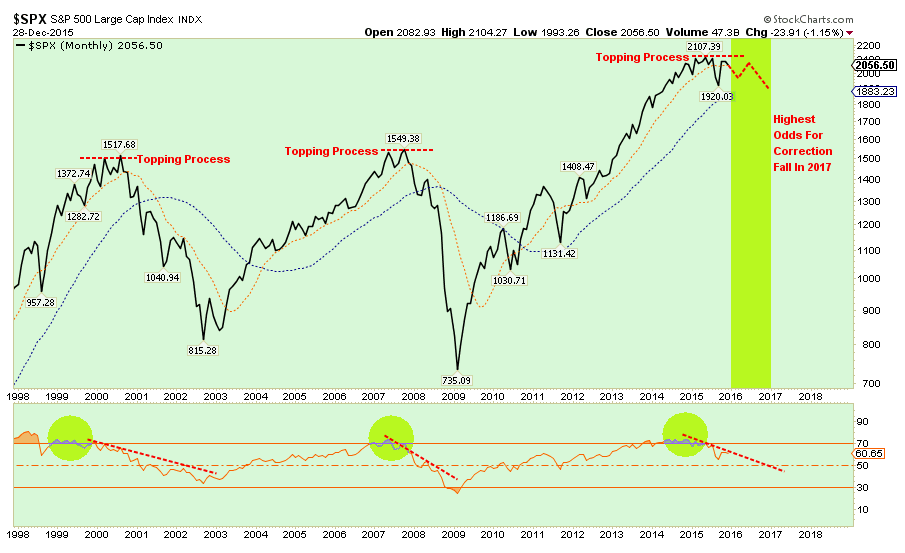

Note that valuations appear to have peaked in the last year which historically has been coincident with market peaks in the past. The next chart shows the many similarities between the current market topping process and the previous two bull-market peaks. With the Federal Reserve now intent on tightening monetary policy in a weak economic growth environment, the odds of a negative return year in 2016 has risen markedly.

However, while 2016 is likely to be a negative return year, it is either late 2016 or early 2017 that the economy slips into a recession and the next major market correction occurs. While that is what the historical statistics suggest, it should be noted that previous market cycles were not operating at the lowest average annual rates of economic growth on record. There are many issues that could advance the recessionary cycle/market reversion into 2016.

MIND THE “E” – earnings, that is.

My most recent posting discussed the historical extremes in P/E valuations currently exhibited specifically by the S&P 500 (recent valuations in the Nasdaq and Russell 2000 are even more extreme than they are in the S&P and Dow). Some of the following excerpts will expose the extraordinary lengths to which corporate CFO’s will go to manipulate earnings and the common earnings per share (EPS) format in which they are reported to the media and the public in order to portray them in the best possible light. Also keep in mind as you read these excerpts that much of the market rally the past couple of years has been driven by corporations borrowing money at historically low interest rates and buying back their own stock, thus reducing the “S” in the EPS calculation and thereby juicing the reported EPS numbers that are put forth.

“Furthermore, the reason that earnings only grew at 6% over the last 25 years is because the companies that make up the stock market are a reflection of real economic growth. Stocks cannot outgrow the economy over the long term…remember that.”

“The Wall Street Journal confirmed as much in a 2012 article entitled “Earnings Wizardry” which stated:

“If you believe a recent academic study, one out of five [20%] U.S. finance chiefs have been scrambling to fiddle with their companies’ earnings. Not Enron-style, fraudulent fiddles, mind you. More like clever—and legal—exploitations of accounting standards that ‘manage earnings to misrepresent [the company’s] economic performance,’ according to the study’s authors, Ilia Dichev and Shiva Rajgopal of Emory University and John Graham of Duke University. Lightly searing the books rather than cooking them, if you like.”

This should not come as a major surprise as it is a rather “open secret.” Companies manipulate bottom line earnings by utilizing “cookie-jar” reserves, heavy use of accruals, and other accounting instruments to either flatter, or depress, earnings.

“The tricks are well-known: A difficult quarter can be made easier by releasing reserves set aside for a rainy day or recognizing revenues before sales are made, while a good quarter is often the time to hide a big ‘restructuring charge’ that would otherwise stand out like a sore thumb. What is more surprising though is CFOs’ belief that these practices leave a significant mark on companies’ reported profits and losses. When asked about the magnitude of the earnings misrepresentation, the study’s respondents said it was around 10% of earnings per share.”

Of course, the reason that companies do this is simple: stock-based compensation. Today, more than ever, many corporate executives have a large percentage of their compensation tied to company stock performance. A “miss” of Wall Street expectations can lead to a large penalty in the company’s stock price.

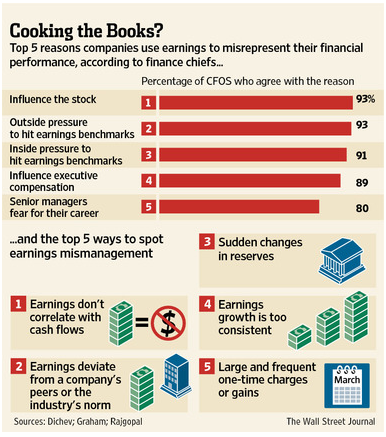

Therefore, it is not surprising to see 93% of the respondents pointing to “influence on stock price” and “outside pressure” as reasons for manipulating earnings.

Note: For fundamental investors this manipulation of earnings skews valuation analysis particularly with respect to P/E’s, EV/EBITDA, PEG, etc.

This was brought to the fore again recently by the Associated Press in: “Experts Worry That Phony Numbers Are Misleading Investors:”

“Those record profits that companies are reporting may not be all they’re cracked up to be.

As the stock market climbs ever higher, professional investors are warning that companies are presenting misleading versions of their results that ignore a wide variety of normal costs of running a business to make it seem like they’re doing better than they really are.

What’s worse, the financial analysts who are supposed to fight corporate spin are often playing along. Instead of challenging the companies, they’re largely passing along the rosy numbers in reports recommending stocks to investors.“

Here are the key findings of the report:

- Seventy-two percent of the companies reviewed by AP had adjusted profits that were higher than net income in the first quarter of this year.

- For a smaller group of the companies reviewed, 21 percent of the total, adjusted profits soared 50 percent or more over net income. This was true of just 13 percent of the group in the same period five years ago.

- From 2010 through 2014, adjusted profits for the S&P 500 came in $583 billion higher than net income. It’s as if each company in the S&P 500 got a check in the mail for an extra eight months of earnings.

- Fifteen companies with adjusted profits actually had bottom-line losses over the five years. Investors have poured money into their stocks just the same.

- Stocks are getting more expensive. Three years ago, investors paid $13.50 for every dollar of adjusted profits for companies in the S&P 500 index, according to S&P Capital IQ. Now, they’re paying nearly $18.”

Mind the “E”, indeed. My advice? Ignore the talking heads, do your own thinking and research, and apply your clarity of thought and analysis to your own personal financial planning not only for 2016 but for many years ahead. Best wishes to all for a happy and prosperous new year!

______________________________________________________________________

General Market Observation: This was an amazing down week for the global markets and a catalyst to stem the current tide may not show up until more of the excess is purged. All three of the Tracking Indexes we followed had the largest one week drop since the indexes started showing topping characteristics almost 15 months ago. Both the NDX and RUT fell more than the SPX which dropped almost 6% for the week. Most of the market drivers came from the China market in combination with other bad news that loaded extra weight on a US market only being held up by a few stocks. As these final strands (stocks) like AAPL and others also turned negative there was nothing to hold the Indexes up. This drop to the downside was very classic of price action just prior to even more significant drops.

I’ll speak to the S&P only tonight because a similar situation can be observed on the other indexes. The weekly S&P chart below shows that price action continued to fail at past support zones and now rest in a strong support zone between 1925 and the 1875 level. The next level of support if 1875 fails is down at lows from 2014 in the area of 1825. Price is becoming more and more oversold and extended from the moving averages. This typically means a bounce or relief rally is in the offing but fake out bounces can also lead to “bear” traps which sucks traders in at a low only to have the bottom drop out for larger losses.

While the market was in the uptrend that started back in 2008 the corrections tended to be short and shallow. The current correction is already 10%+ down from highs in the 2134 range. It appears that the corrections are getting deeper with weaker rebounds which is sign of weakness. A lower high is now in place and price action is accelerating to the downside. If support fails at 1866 we could see price stair step down to 1577 the high from 2007. This level is only 17% away from Friday’s close. Apply the rule of thumb that price go down 2/3’s faster than they go up if the correction intensifies price could reach 1577 in about 250 days or mid-September. I’m not making a prediction of future market action only assessing a potential move based on proven technical analysis.

Armed with these observations a long trade on the indexes or individual stocks must be very compelling going forwarded. A more prudent tact will be to wait rebounds to resistance identified on weekly and monthly charts to plan short trades. Secondly I will be patient with my objective to build a portfolio recognizing the headwind for this objective seems to be strong.

SPX: Downside Market Short the SPY or SPY Puts. Preferred ETF’s: SPY, UPRO and SPXL

NDX: Downside Market Short the QQQ or QQQ Puts. Preferred ETF’s: QQQ and TQQQ

RUT: Downside Market Short the IWM or IWM Puts. Preferred ETF’s: IWM and TNA

The Early Warning Alert Service has hit all eight major market trading point this year. See the updated video at: https://activetrendtrading.com/early-warning-alerts-2/

If simplifying your life by trading along with us using the index ETF is of interest you can get the full background video at: https://activetrendtrading.com/etf-early-warning-alerts-video/

The How to Make Money Trading Stock Show—Free Webinar every Friday at 10 a.m. PDT. This weekly live and recorded webinar helped traders find great stocks and ETF’s to trade with excellent timing and helped them stay out of the market during times of weakness.

How to Make Money Trading Stocks on Friday, Jan 15th

Register Here: https://attendee.gotowebinar.com/register/1285247001330231553

To get notifications of the newly recorded and posted How to Make Money Trading Stocks every week subscribe at the Market Tech Talk Channel: https://www.youtube.com/channel/UCLK-GdCSCGTo5IN2hvuDP0w

- The Active Trend Trader Referral Affiliate Program is ready. For more information or to become an Affiliate please register here: https://activetrendtrading.com/affiliates-sign-up-and-login/

_______________________________________________________________

Index Returns YTD 2016

ATTS Returns for 2016 through Jan 8, 2016

Percent currently invested of $100K account: Strategies I & II invested at 0%; Strategy III invested at 20%

Active Trend Trading’s Yearly Objectives:

- Yearly Return of 40%

- 60% Winning Trades

- Early Warning Alert Target Yearly Return = 15% or better

For a complete view of specific trades closed visit the website at: https://activetrendtrading.com/current-positions/

Updated first full week of each month.

___________________________________________________________

For our all Active Trend Trading Members here’s how we utilize our trading capital

Trading Capital Setup and Position Sizing: Every year we start the year off trading a $100K margin account split up into the three strategies used with the Active Trend Trading System.

- Each trader must define their own trading capital in order to properly size trade positions to meet their own risk tolerance level!

- Strategy I: Capital Growth—70% of capital which equates to $140K at full margin. This strategy trades IBD Quality Growth Stocks and Index ETFs. Growth Target 40% per year.

- Strategy II: Short Term Income or Cash Flow—10% of capital or $10K. This strategy focuses on trading options on stocks and ETF’s identified in Strategy I. The $10K will be divided into $2K units per trade.

- Strategy III: Combination of Growth and Income—20% of capital or $20K. This strategy will use LEAPS options as a foundation to sell weekly option positions with the intent of covering cost of long LEAPS plus growth and income.

- The $70K Strategy I portion of the trade account is split between up to 4 stocks and potentially a leveraged Index ETF. Actual number of shares will vary of course depending on price of the entity traded and amount of margin available. We have found that limiting open positions to only 5 entities greatly reduces the trade management time requirements for members.

- Naked Puts or short term options strategies will be used occasionally for Income Generating Positions

- None of the trade setups are recommendations to trade only notification of planned trades from set ups using the Active Trend Trading System. Each trader is responsible for establishing their own appropriate risk level if they decide to parallel trade.

- The Active Trend Trading System objective is to provide a clear and simple system designed for members who work full time.

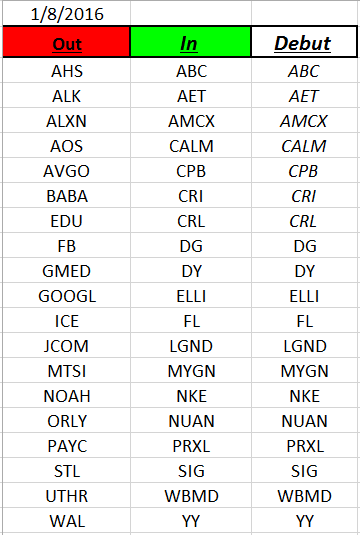

Outs & Ins: In all the years I’ve been following the IBD 50 & 100 I’ve never seen a wholesale swap out of stocks. On the last two updates 27 of the stocks that started on the first list of 2016 are OUT! Even with the markets getting weaker and appearing like they are headed for a significant correction it is important to keep up with the IBD 50 and the Running List. Some stocks on the list will turn up prior to the market thus it becomes a good pre-warning list for when strength is moving back into growth stocks. This often precedes the market turn by several weeks or longer. Remember we know that the IBD 50 is where the big fish swim!